Thailand Branded Residences: Global Strategy 2026 –2030

The Global Capital Shift to Thailand

Thailand's Position in the Global Branded Residences Market (2026 –2030)

This article is part of our Branded Residences Global Investment Series – a multi-part research framework examining structure, risk, yield, and exit logic across global branded residential markets.→ (Read Parts 1 Branded High-Growth Investment & Due Diligence )

During 2024–2025, the global Branded Residences sector has clearly entered a phase of market maturity.

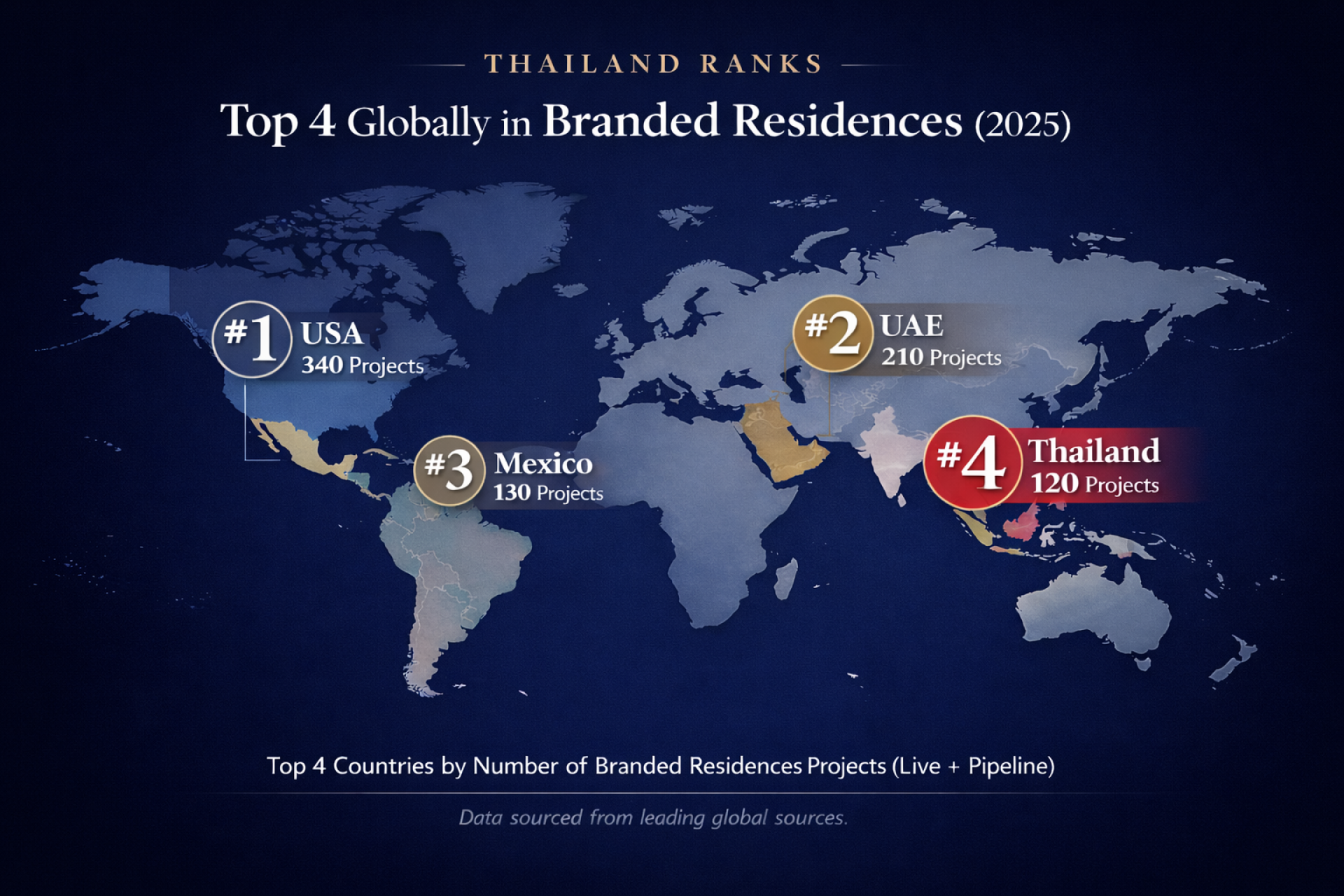

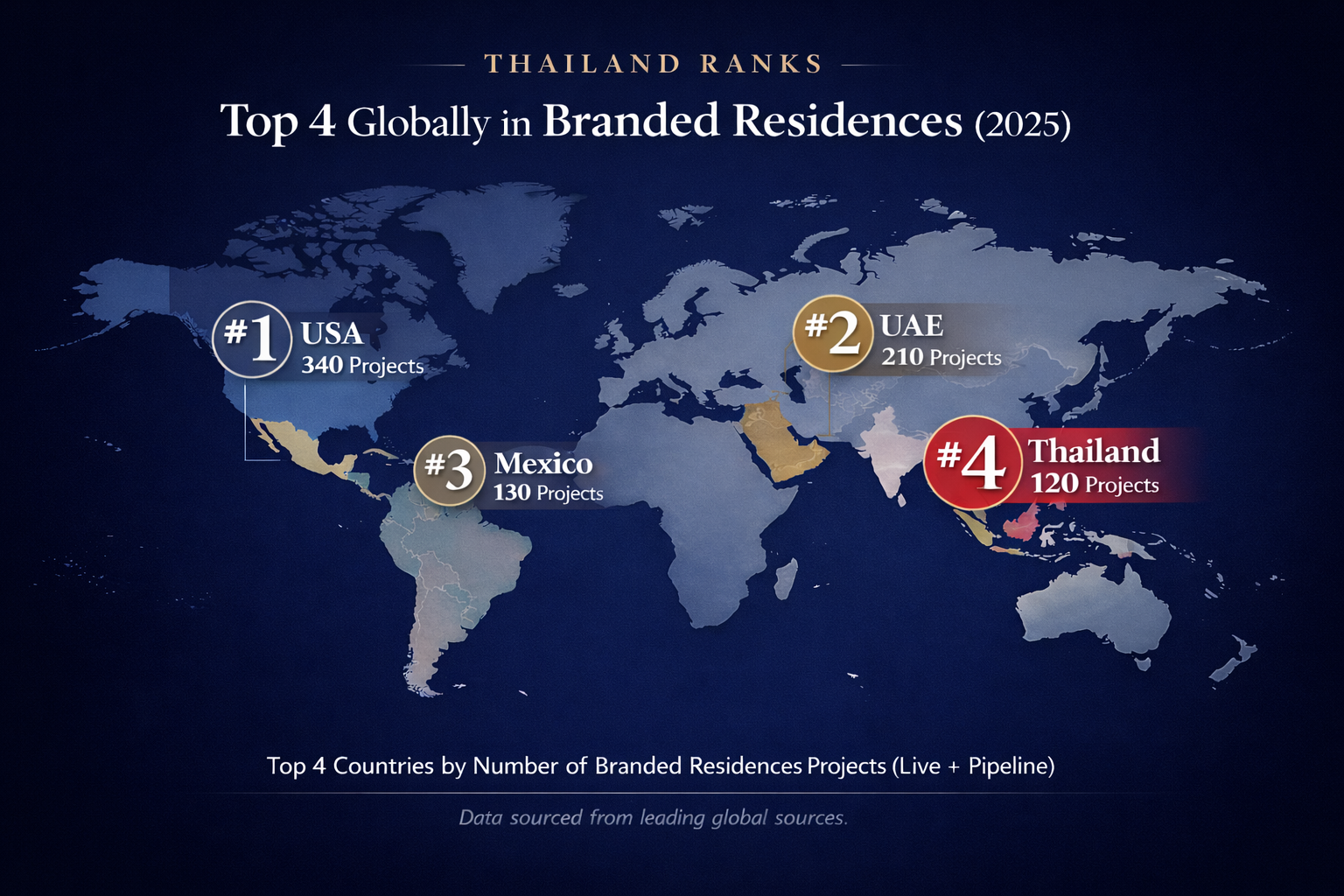

According to leading global real estate research houses such as Knight Frank, Savills, and C9 Hotelworks, Thailand now ranks among the Top 4 countries globally in terms of the number of Branded Residences projects, including both live developments and projects in the pipeline.

Thailand now sits alongside the United States, the United Arab Emirates (UAE), and Mexico–markets long recognized as global leaders in branded real estate.

Graphic 1: Top 4 Globally in Branded Residences (2025)

The significance here is not merely the ranking itself, but what it confirms:

- Thailand is no longer an alternative or fringe market

- It has become a mainstream global destination for branded luxury real estate

- The market demonstrates real liquidity and a functioning secondary market

- It now exceeds many emerging peers such as Vietnam and Indonesia, which remain in an early-stage development cycle

For investors, this signals market maturity, diversified buyer demand, and clearer exit pathways.

Graphic 2: Resale Premium 40–80%

Market estimates based on public listings & global brokerage benchmarks

Price ranges are indicative benchmarks, not extracted from a single published table

What this shows

Global research and market benchmarks indicate that branded residences in Thailand can achieve resale premiums of approximately 40–80% compared to non-branded projects in comparable locations.

Why it matters

This highlights the role of brand as a liquidity engine.

For medium- to long-term investors, secondary market confidence and exit visibility are as critical as initial yields.

What to watch out for

Not all branded projects perform equally.

Brand quality, post-handover property management, and real secondary buyer demand remain decisive variables.

How Professional Investors Decide

They don’t ask: Is this project good?

They ask:

• Is the exit predictable?

• Is liquidity defensible?

• Is downside protected?

If you’re evaluating Phuket property seriously,

you should review your position with a professional framework.

→ Request a private investment consultation

Asset Management / Rental Program

For income stability during the holding period, the underlying structure of guaranteed return programs often matters more than headline yield. → Deep dive: Guaranteed Return Strategy for Branded Residences

Yield vs Capital Appreciation

While long–term capital appreciation is primarily driven by the 40–80% resale premium associated with strong global brands, the hotel-managed operating structure plays a critical role in generating professional, risk-adjusted yield during the holding period.

This dual dynamic allows branded residences in Thailand to function not merely as lifestyle assets, but as truly passive global investments combining income stability with exit-driven upside.

The Price Gap Thesis: A Global Arbitrage Opportunity

The same global arbitrage logic applies beyond Thailand.

→ Asia Arbitrage Case Study: Why Japan’s MUWA Niseko Completes Your Asia Investment

At the core of this macro analysis lies a single question:

How are comparable global assets priced across different countries?

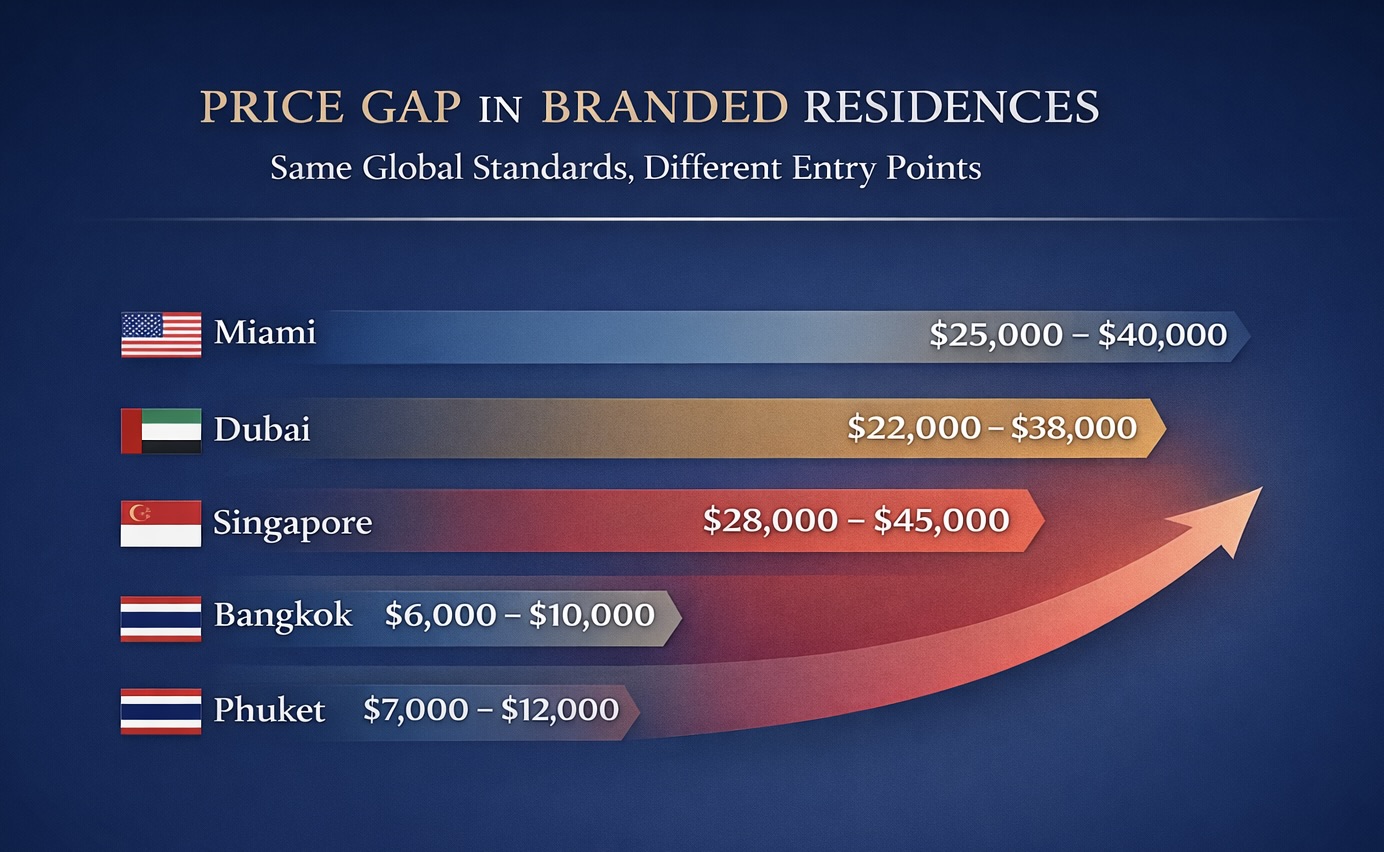

Graphic 3: Price Gap (USD/sqm Comparison)

Market estimates based on public listings & global brokerage benchmarks

Price ranges are indicative benchmarks, not extracted from a single published table

Comparable Branded Residences Pricing (USD/sqm)

| City | Avg. Price (USD/sqm) | Notes |

| Miami | 25,000–40,000 | Waterfront / Iconic Brands |

| Dubai | 22,000–38,000 | Ultra-luxury, Global Safe Haven |

| Singapore | 28,000–45,000 | Limited supply, high taxation |

| Bangkok | 6,000–10,000 | Low global brand entry price |

| Phuket | 7,000–12,000 | Resort & lifestyle-led demand |

What this shows

Thailand–particularly Bangkok and Phuket–continues to offer significantly lower entry pricing compared to mature global markets such as Miami, Dubai, and Singapore, despite comparable brand standards and service quality.

Why it matters

This pricing disparity represents what institutional investors refer to as Global Arbitrage–acquiring globally comparable assets in markets where prices have not yet fully reflected long-term potential.

What to watch out for

Lower prices do not guarantee superior returns.

Location quality, contract structure, management model, and surrounding supply remain decisive.

Key interpretation:

Lower pricing is not a guarantee of profit

it represents an open opportunity, provided that:

- The location is structurally sound

- Contracts are transparent

- Yield programs are verifiable

- Genuine secondary demand exists

Safe Haven & Ownership Advantage

In an era of heightened geopolitical volatility, global capital no longer flows toward a single destination.

Thailand is increasingly viewed as a neutral geopolitical ground, allowing capital from Europe, Russia, China, and the Middle East to enter with relatively low political or policy friction.

Ownership Structure Comparison

| Country / Region | Ownership Type | Stability |

| Thailand | Freehold Condominium | High |

| Bali | Leasehold | Low |

| Vietnam | Limited foreign quota | Low |

| UAE | Designated freehold zones | Medium |

| Singapore | Freehold / Leasehold | High (but very high pricing) |

For long-term investors, these differences directly affect:

- Exit value

- Transferability

- Intergenerational asset security

Transaction Costs & Tax Efficiency

Beyond ownership structure, entry costs play a meaningful role in capital efficiency.

Thailand's transaction costs (transfer fees and taxes) remain significantly lower than in markets such as Singapore, where Additional Buyers Stamp Duty (ABSD) materially increases acquisition costs for foreign investors.

This structural advantage further enhances Thailand's Global Arbitrage appeal, particularly for investors evaluating net capital deployed versus long-term value realization.

2025–2030: From Hotel-Branded to Lifestyle & Wellness Ecosystems

Historically, Branded Residences were designed primarily for leisure and hospitality use.

Between 2025–2030, the sector is transitioning toward Lifestyle, Wellness, and Longevity ecosystems.

Brands are no longer just logos–they are becoming part of integrated living, healthcare access, and long-term residency solutions.

Case Study: Phuket–From Tourist Destination to Global Residence

Phuket’s long-term IRR is driven by its ecosystem structure, not tourism alone.

→ Deep dive: Ecosystem Effect Value: Why Phuket Real Estate IRR Hits 17%

- Emergence as Asias Medical & Wellness Hub

- Phuket International Airport Expansion (Phase 2)

- Growing long-term residency among High Net Worth Nomads

These factors are transforming "tourists" into global residents, supporting more durable and higher-quality demand.

Capital Source Mapping: Who Are the Real Buyers?

Thailand's branded residential market is supported by diverse capital sources, each driven by different motivations:

| Capital Source | Primary Motivation |

|

Europe |

Wealth preservation & lifestyle |

| Russia / CIS | Safe haven & diversification |

| China | Capital parking & family use |

| Middle East | Yield & brand-driven assets |

| Singapore / Hong Kong | Capital efficiency & liquidity |

This diversity reduces market risk and enhances long-term liquidity.

Institutional Lens: How Professional Investors Think

Brand value is only proven at exit. → Review: Liquidity & Exit Strategy

Institutional investors assess Branded Residences differently from retail buyers, with a strong emphasis on secondary market liquidity.

According to Savills Research (2025), branded projects in Thailand demonstrate 40–80% resale premiums over non-branded peers due to:

- Trust standard: reduced uncertainty in quality and maintenance

- Global resale reach: access to international buyers

- Inflation hedge: superior pricing power

Risks That Even Branding Cannot Fix (Honesty Premium)

Investors should remain aware that:

- Branding cannot correct poor location choices

- Branding cannot offset structural oversupply

- Branding does not guarantee yield unless contractually defined

- FX and political risks remain

- A secondary market requires real buyers, not assumptions

Decision Matrix: Turning Insight into Strategy

| Objective | Thailand Branded Residences |

| Long-term IRR | Strong |

| Capital preservation | Strong |

| Liquidity | ModerateStrong |

| Lifestyle utility | Strong |

| Institutional grade | ModerateStrong |

Global Branded Residences: Market Snapshot (Live + Pipeline)

According to the Knight Frank Global Branded Residence Survey:

- Over 1,000 projects globally

- Across 80+ countries

- Hotel-linked: ~80–82%

- Standalone branded: ~18–20%

- Non-hotel brands (automotive, fashion, lifestyle): ~15–20% (growing pipeline)

Key interpretation:

Global statistics illustrate market direction, not guaranteed investment outcomes.

Neutrality Statement

The following resources support strategic investment decisions.

References

- Knight Frank – The Global Branded Residence Survey 2025

- C9 Hotelworks – Asia Branded Residences Market Review 2025

- Knight Frank – The Residence Report 2025

- Savills – Research Branded Residences Insights

Serious about your investment position?

If you would like independent insights or wish to explore pre-vetted opportunities aligned with your objectives, I work directly with private investors on entry structure, risk control, and exit logic.

→ Request our Global Vetting Report

→ Schedule a confidential consultation

We focus on structure, risk, and exit logic — not sales pressure.

Secure the right asset, at the right time, with the right framework.