Capital Defense: Luxury Real Estate Risk & Scenario Planning

Capital Defense in Thailand Property Cycles

A Structural Approach to Protecting Principal in the Phuket Luxury Property Market

Capital Defense as the Core of Sustainable Property Investing

Capital Defense sits at the heart of sustainable real estate investing.

It is the discipline of designing a principal protection system before the acquisition decision–through structural risk analysis, stress testing, real demand validation, and professional asset management.

The objective is simple but uncompromising:

to ensure that the investment portfolio survives and preserves value across all economic cycles, particularly in cyclical markets such as the Phuket luxury property market.

The Question Investors Ask Most Often

The most common question serious property investors ask is not:

“What return can I expect?”

But rather:

“If events do not unfold as expected, how is my principal protected?”

This article is written to answer that question directly–within the context of Phuket’s luxury residential market:

a market with strong long-term fundamentals, yet pronounced property cycle volatility.

To ground the analysis in reality, we use a single, representative case:

A THB 15 million luxury condominium in Phuket.

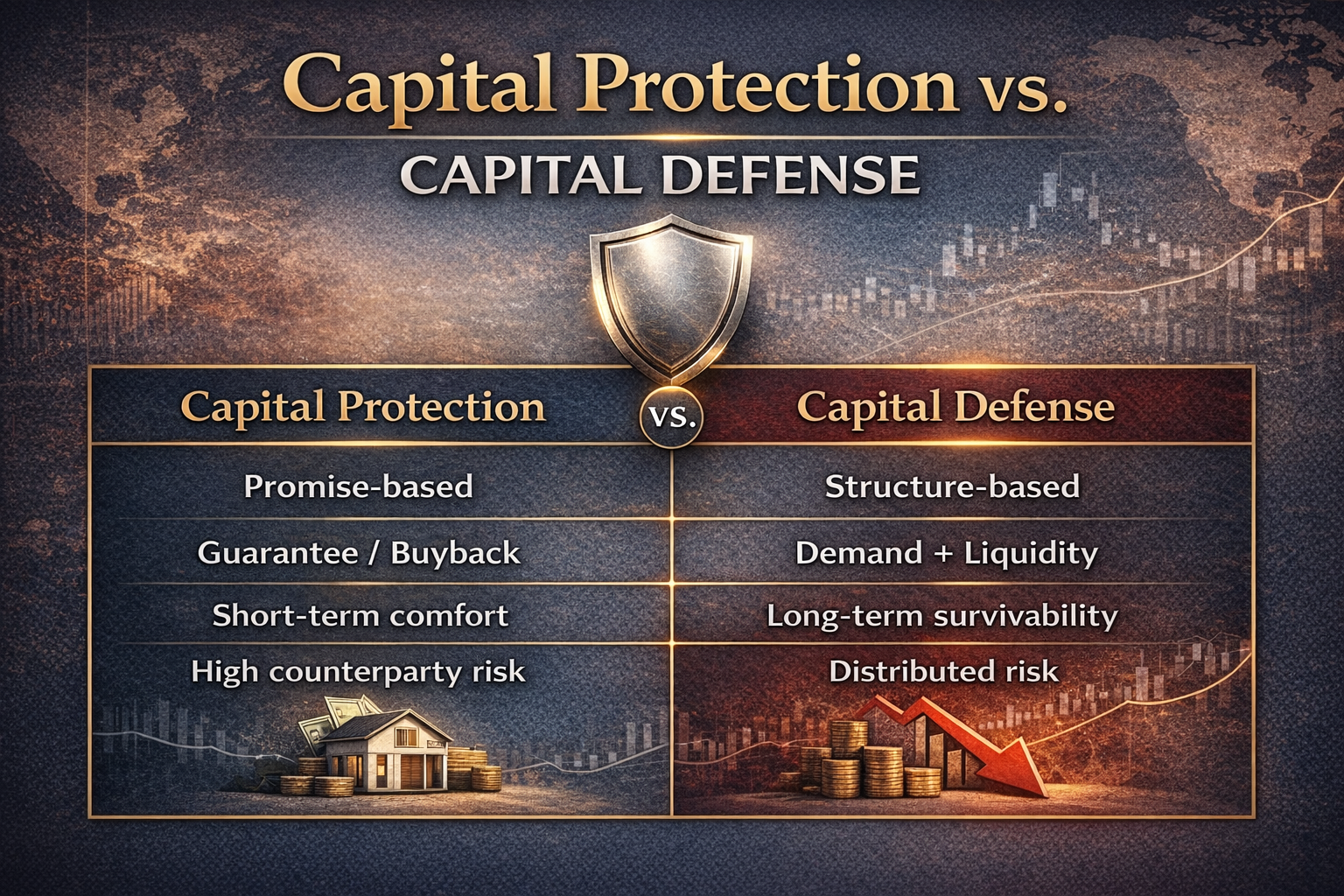

What Capital Defense Is–and What It Is Not

Capital Defense is the deliberate design of an investment to survive worst-case scenarios.

It does not rely on:

- Guarantees

- Buyback promises

- Sales-driven assurances

This article focuses on Defense by Structure, not Defense by Promise.

In market cycles, waiting is not always a defensive strategy. Review the risk implications in The Real Cost of Waiting.

Real Risks in the Phuket Luxury Property Market

Market Drawdown: Price Declines Are Real

While Phuket demonstrates long-term recovery potential, downcycles are inevitable.

During market contractions:

- Transaction prices may decline 20–40%

- Resale liquidity can extend to 12–24 months

Common compounding factors include:

- Temporary rental demand disruptions

- Ongoing holding costs that quietly erode principal

So what?

When these risks materialize simultaneously, does your asset survive?

Comparative Case Study: THB 15 Million Investment

| Analysis Factor | Scenario A: No Capital Defense | Scenario B: With Capital Defense |

| Purchase Price | THB 15,000,000 | THB 15,000,000 |

| Asset Structure | Design-driven / brochure-led | Demand + liquidity-driven |

| Normal Annual Rental Yield | 4% = THB 600,000 | 5.5% = THB 825,000 |

| Total Annual Costs | 3% = –THB 450,000 | 2.5% = –THB 375,000 |

| Net Cash Flow (Normal Year) | +THB 150,000 | +THB 450,000 |

| Stress Test: –40% Rental | –THB 90,000 loss | +THB 120,000 positive |

| Unable to Sell | 24 months | 24 months |

| Cumulative Cash Flow (24 months) | –THB 180,000 | +THB 240,000 |

| Market Drawdown (–25%) | Value ≈ THB 11.25m | THB 12–12.5m (demand-supported) |

| Forced Sale Risk | High | Low |

| Principal Outcome | –20–25% erosion | ~0–8% loss or preserved |

Is your asset a Speculative Risk or a Capital Defense? Don't wait for a market drawdown to find out. Get a structural stress-test analysis for your Phuket portfolio. [ Check My Portfolio Defense ]

What Investors Must Understand

- Risk does not come from price declines alone, but from being forced to sell at the wrong time

- Assets that remain cash-flow positive under stress are true capital-defense assets

- If “selling” is the only exit, the asset is speculative by nature

A capital-defense asset must offer options beyond selling:

- Ability to shift tenant profiles (tourism → long-stay)

- Rental income that truly covers holding costs

- Freedom from decision-making under financial pressure

If you can hold, your principal is not forced to disappear.

In practice, Capital Defense collapses immediately if the asset lacks secondary-market liquidity.

A deeper structural analysis of exit pathways and buyer pools is explored in Liquidity & Exit Strategy.

Regulatory & Legal Risk

For foreign investors, price risk is only part of the equation:

- Unclear ownership structures (leasehold vs freehold)

- Nominee risk

- Improper Foreign Exchange Transaction (FET) documentation

So what?

Assets with opaque legal structures lose global liquidity instantly.

The Invisible Shield: Plugging Capital Leakage

Beyond the asset itself, investors often underestimate:

- Tax & Exit Cost Planning–designed from day one, not at sale

- Currency & Repatriation Risk–valid FET documentation enables capital return

- Insurance & Loss-of-Rent Coverage –stabilizes cash flow

a frequent blind spot for international investors.

A structural breakdown is covered in Tax Strategy & Risk Mitigation.

Footnote: Exit Tax Risk

If a property in Thailand is sold within five years, Specific Business Tax (SBT) may apply at approximately 3.3% of the assessed or sale price (whichever is higher).

This represents a significant transaction cost that directly erodes principal if not planned in advance.

Speculative Asset vs Capital Defense Asset

| Factor | Speculative Asset | Capital Defense Asset |

| Exit Strategy | Sale only | Rent / Hold / Sell |

| Cash Flow | Negative or guaranteed |

True net yield |

| Management | Short-term | Professional, long-term |

| Buyer Pool | Narrow | Broad, global |

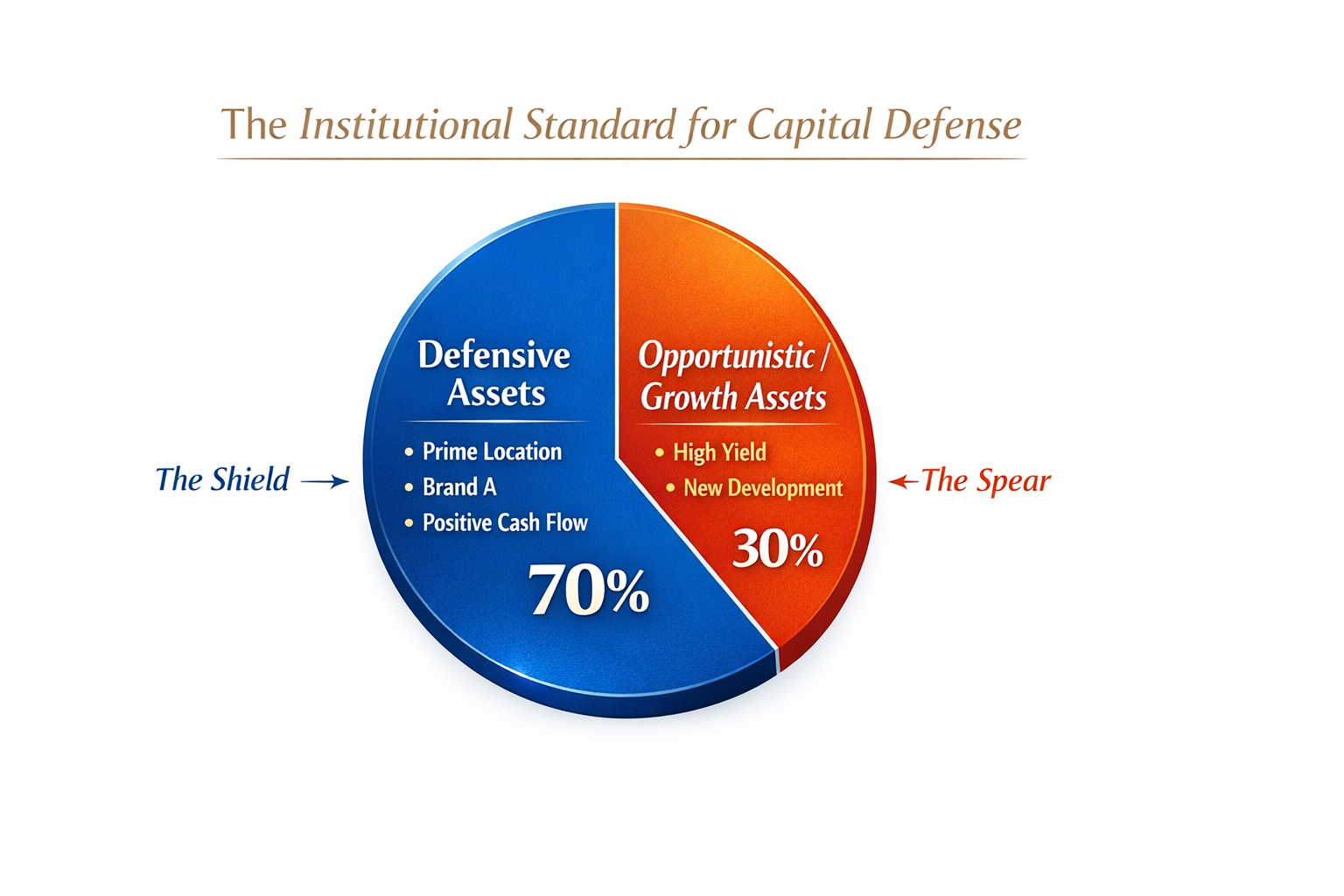

Developer Risk & the 70/30 Rule

Developer risk does not end at construction–it continues through post-sale incentives.

A strong brand is not marketing—it is principal collateral.

The Institutional 70/30 Allocation Rule

- 70% Defensive Assets (prime locations, strong brands)

- 30% Opportunistic Assets (growth-driven upside)

The Advisor’s Role: Strategic, Not Transactional

- The Filter–rejecting misaligned deals

- System Thinking–post-purchase reality over brochures

- Alignment of Interest–protecting portfolios, not sales volume

At Angie Phuket Residences, we don't just sell property; we engineer capital defense systems. Learn how our independent vetting standards protect your principal. [ Meet Your Investment Strategist ]

Capital Defense Is a System, Not Hope

Capital protection means preparing for worst-case scenarios.

If you cannot sell within 24 months, can your asset still defend its principal?

Professional investors do not win by always being right.

They win by not losing badly when they are wrong.

However, no defense system works without post-transfer asset management capable of controlling real cash flow and costs–explored in Post-Purchase Reality: Who Manages the Asset After Transfer?

At the global portfolio level, Capital Defense is not solely about asset quality.

It is about a country’s position within global capital allocation.

Institutional investors prioritize markets that:

- Exhibit real end-user demand

- Offer transparent legal and ownership frameworks

- Provide branded, professionally managed assets

- Maintain liquidity through downcycles

Within this framework, Thailand’s luxury property market–particularly Phuket–is no longer viewed merely as a tourism play, but as a strategic allocation within Asian real estate portfolios.

A deeper institutional analysis can be found in:

Thailand’s Position in the Global Branded Residences Market (2025–2030)

Capital Defense is therefore not just about loss prevention–it is about positioning assets correctly within the global capital system.

What You Gain from This Article

If you’ve read this article to this point, you haven’t just gained a better understanding of the Phuket property market.

You’ve fundamentally reframed how real estate investment should be evaluated–at a system level.

You will learn:

- How capital can be eroded even when a project looks attractive and the market itself has not collapsed

- Why cash flow under stress matters far more than brochure-level yield projections

- How to distinguish a Speculative Asset from a true Capital Defense Asset

- Whether an asset can actually survive if it cannot be sold for 12–24 months

- How often-overlooked costs–taxes, exit costs, and liquidity constraints–quietly destroy principal

- Why institutional investors prioritize structure over promises

- And why Phuket is increasingly viewed as a strategic allocation within Asian real estate portfolios

This article was not written to tell you what to buy.

It was written to help you avoid buying what you shouldn’t.

Exclusive Capital Defense Review

If you want to assess whether your asset or portfolio can truly protect principal under scenarios such as:

- Inability to sell for 12–24 months

- Rental income declining 30–40%

- Market drawdowns

[ Claim Your Exclusive Capital Defense Review ]

References (Conceptual & Institutional)

- International Monetary Fund (IMF) –Global Property Cycles

- Bank for International Settlements (BIS) –Asset Price Volatility

- CFA Institute–Capital Preservation & Drawdown Risk

- Bank of Thailand–Property Market Insights

- Yale Endowment Model–Portfolio Allocation Principles